Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Washington This Week CSPAN November 24, 2013 3:00am-5:01am EST

3:00 am

the other in contrast most directly affects term premiums. as the fed buys a larger share of the stock, the quantity of the securities available for private sector portfolio declines. as the security is are just, they should become more valuable . consequently, their yield should follow as investors demand a premium for holding them. . . .

3:34 am

one is talking about what happened before the affordable care act. if we could take our seats

3:35 am

and welcome to this important hearing this morning. the purpose of today's hearing is to explore the success stories of the rollout of the affordable care act in states throughout the country, where teamwork and cooperation has proven to be exceedingly effective. we will also hear from a federal panel that will talk about the federal rollout and some of the challenges that have presented themselves. normally, we have the federal panel first and the state panel second, but at the discretion of the chair, i reversed it, but require the federal leaders to be here to hear from the state exchanges and from individual business owners about how the situation could be improved. i'd like to begin by quoting, i think it was mark twain, who said, "a lie can get halfway around the world before truth gets out of bed in the morning and puts its boots on."

3:36 am

so this morning, we're going to try to give truth a chance. thank you for joining us for this hearing. the affordable care act passed, as we all know, on march -- in march of 2010 and was signed into law by the president three days later. that was over three and a half years ago. last year, the supreme court upheld one of the essential components of this law, the no free rider provision, requiring full participation through private and public health insurance marketplaces. the goals of the affordable care act at the time we passed the law were implemented for creating a workforce that was healthy, because only a healthy workforce can be a strong workforce, and america needs the strongest workforce we can get, so we can continue to have the strongest economy in the world. those were the goals three and a half years ago. that is the hope and promise today.

3:37 am

there were four specific goals of the affordable care act. one, to slow skyrocketing health care costs and reduce what america spends on health care as a share of our gdp. it was rising from 15% to 16.5% and headed very soon to 19%. that trend has been reversed. to use the power, not of the government, but of the private sector competition, the proven power of private sector competition, to rein in costs and improve quality care and coverage. to provide the first opportunity in the history of our country, whether union or nonunion, middle, high, or low-income wage earner, whether self employed, small or large business, to excess affordable, quality health care. and, one of the most exciting and underappreciated features of

3:38 am

the affordable care act, and one that this committee has focused a great deal of work, is that it provided for the first time a key to americans to unlock them from job lock, which prevents individuals in every state, including my own, from starting a new business because the risk associated with leaving full and good employment with full and good health care coverage causes them to stay sometimes in companies where they themselves might even do a better job starting their own, providing disruptive technology or good services. i'm proud to hand many of our entrepreneurs that key and intend to do so. according to the robert wood johnson foundation, nearly 1.5 million americans, including 25,000 louisianans will become self employed thanks to this bill, allowing them to fulfill

3:39 am

their dream of becoming an entrepreneur, to pursue their dreams, to create the product or the system or service that they have dreamed about, and have health insurance, which was not possible before the affordable care act. fourth, to provide coverage to millions of low income and working class families that work 40, 50, and 60 hours a week, and worked for decades, and yet could not afford health care in the united states of america. the way that this bill has been crafted, they will, if the governors would expand medicaid to be able to choose their hospitals, doctors, and have health care. unfortunately, many of our governors are standing in the way. this is the hope and vision that we fought for. it is still worth fighting for now. the focus of today's hearing will be specifically, though, on coverage options and access to our small businesses or businesses regardless of size.

3:40 am

and i want to be clear, this is about the self employed, about the growing percentage of our population that call themselves contractors because of the way our economy is structured to be very flexible and independent. small businesses below 50 and small businesses above. now, we all know the rollout of the federal marketplace for individuals has not worked as well as we had hoped. we know there are many challenges, we will hear about those today. but thank goodness there are bright examples throughout the united states where the aca's vision is working, and we are going to hear from those states today. specifically, we're going to hear from representatives leading the implementation of the s.h.o.p. marketplaces now open at the state level to understand both the challenges and the successes experienced by those states, who accepted the responsibility to build their own exchanges, who accepted the

3:41 am

challenge of the federal government to say we can't always do things right, here, we'll give you the option to do it. some of our governors were brave enough to do so, others were not. usually, this committee hears from federal officials, as i said, but i've asked them specifically to be in the room, because they need to hear the best practices about what's going on around the country so they can get a better understanding of what we're trying to do. we will also be hearing from representatives, federal agencies, et cetera. now let me go into a few more things and the time that i take will be given equally to the minority. before we begin, i'd like to take a moment to put today's discussion into context. as we were debating the health reform act in 2009, and i was here and robustly engaged in that debate and helped to design the system that we have now, which was a compromise system between a government-run single payer system and a medical savings account system with no

3:42 am

floor or no safety net, we designed this. it was particularly for 96% of all businesses that employ fewer than 50 people, who were struggling to remain competitive and we were focused on helping them. small businesses were paying an average of 18% more than big business for health insurance that wasn't the same quality, and they saw their health care costs increase faster than the prices of the products and services they were selling. the record says four times faster than the rate of inflation between 2001 and '09, after the number of employees offering coverage remained relatively flat in the 1990s, average annual family premiums for workers at small businesses increased by 123%, from 5,700 in 1999 to 12,700 in 2009, so the rate of increase was going up

3:43 am

substantially before the affordable care act, which is one of the reasons it was passed, to try to taper down those rates and get them lower. the percentage of small firms offering coverage started falling from 65% to 59%, and it was spiraling downward. it's no wonder that since 1986, one concern for every small business every year has been access to affordable care, and this is not from a liberal think tank, this is the finding of the national federation of independent business. they have testified before our committee on many occasions. this made reform, in my mind, imperati imperative, and the small business marketplace an important tool towards increasing choice and competition, reducing cost for small business, and providing coverage to their employees that serve as the back bone of this american economy and a model for

3:44 am

the world. a shop is an online marketplace where small businesses with 50 or fewer employees can purchase health insurance from their employees voluntarily, because under the affordable care act, they are not required, the businesses aren't required, the employees can. functioning s.h.o.p. marketplaces will give functioning business owners the tools they need to be smart consumers as they choose affordable options for their businesses without damaging their bottom line and leveling the playing field with large businesses to improved access to affordable health benefit options to their employees. many are like family. i cannot tell you how many small business owners have come up to me over the course of the last several years and said, senator, i would love to offer my people insurance, but i cannot find it anywhere, and because my best friend who helped me start this business wife has cancer, we are now completely priced out. how am i going to keep my

3:45 am

business, because i feel badly, because i don't want to ask him to leave. if he would leave, i could get employment -- i mean, insurance, for my businesses. that's a choice i don't think americans should be making, and i don't want anyone in louisiana to make that choice or have to make that choice. at the end of this month, small businesses with 50 or fewer full-time equivalent will be eligible but not required to purchase and provide insurance for their employees. pooling these eligible or e.t. small businesses and larger groups will spread risks, allowing insures to stop providing high premiums. the new s.h.o.p. marketplaces will allow small businesses to compare plans easily, which was never hardly ever possible before, taking the administrative burden off

3:46 am

employers and allowing them to get back to running their businesses, which they do best, not filing paperwork to get health insurance. it was a broken market, we intend to fix it. according to 2009, business round table report, the administrative cost to small businesses through the exchanges would be reduced by as much as 22%. i'd like my staff to put up what's happening around the state and i'd like people's eyes to focus what's happening in a good way and still challenging ways. this is the united states of america, you will recognize it. declared state-based exchanges are in red. planning for partnership exchanges are in the gray area, and those states that defaulted to the federal government, and i want to underscore this, because mine is one of them, states that had a chance to set up an exchange for their small businesses that were given every opportunity and in the case of

3:47 am

my state was also attached with a check for $16 billion to help make it work, was rejected by my governor and by many governors, and instead, they defaulted at their own choice, their own choice, not at president obama's choice, and then did nothing virtually to help. it's no wonder some of them aren't working, but today, we're going to have an opportunity to talk to those governors, both republicans and democrats that did step up and lead, did take what was offered to them and set up exchanges that would work for their small businesses. each state has the flexibility to decide how they want to operate their health insurance marketplaces. as you can see on this map, there are four different categories that each of the 50

3:48 am

states and the district of columbia fit into. some states have federally facilitated exchanges, which means they are leaving it to the federal government, unfortunately, that would be mine. i wish i had been given that choice, but that was one mistake in the bill, leaving it up to governors, maybe not a mistake, but in some cases it was, it seems. other states are operating partnership exchanges where the federal government operates the marketplace in conjunction with the state. some states chose to do a partnership with the federal government, we'll see how that's working. another group of exchanges have split exchanges, where the federal government runs the individual marketplace and the state runs the s.h.o.p. marketplace. the final category is made up of states that run both, these states cover approximately 1/3 of the population of the united states. this is a big country. and it goes way beyond the beltway of washington, d.c., and you're going to hear today about one-third of the population that it's either working really,

3:49 am

really well or it's working to some degree and with some changes could work better, and a few places where they are having some serious challenges, but you're going to hear from people who are at least trying. kentucky and the district of columbia are included in this category, and we will be hearing from representatives of these exchanges during our first panel this morning. in total, there are 18 states, plus the district of columbia, running their own s.h.o.p. exchanges, and for the record, since this is so important, i want to put these states in the record, california, colorado, connecticut, the district of columbia, not a state yet, maybe one day, hawaii, idaho, kentucky, maryland, massachusetts, minnesota, nevada, new mexico, new york, oregon, rhode island, utah, vermont, and washington state. in all parts of our country, some with republican governors, some with democratic governors, but all with people who need leadership to help them find

3:50 am

health care that they can afford. and it makes up nearly 40% of all the nation's small employers are in these states. that's who we're focused on today. we all know that the rollout of the individual insurance website has been disappointing, to say the least, but today's hearing is focused on implementing the rollout of the s.h.o.p. exchanges, which is the focus of our committee, where we had a lot of input into how this bill was designed, to emphasize the need for a better rollout, not just for individuals, but for small businesses. today, as i said, we are joined by states that accepted this challenge and responsibility to create state-based exchanges and did it well, as well as those who are having difficulty. for those states that have made the decision to operate their own s.h.o.p. marketplaces, we're already seeing evidence. i'm not going to repeat everything that's in testimony, but i will say for kentucky, i was completely happy to see and spoke to senator -- governor

3:51 am

bashir, kentucky did what i thought we should do, and i have a bill to correct this, to use their licensed health agents to sell the policies, which is a brilliant idea. we did not do that. unfortunately. and so they hit the ground running because their agents were already licensed and understood the market well and were able to sell. we'll hear more about that. that's kentucky, and you'll hear more about kentucky. in d.c. between october 1 and 13, they had more than 84,000 visitors to their website. what i loved about the testimony from d.c., and we'll hear more about it, is that instead of the chamber of commerce dragging its feet, he says, the d.c. chamber of commerce, the greater washington area hispanic chamber, and the restaurant association partnered to build this exchange and put their muscle and their brainpower behind it, and it's probably one of the most successful in the country. nearly 700 employer accounts

3:52 am

have been created using their site, and finally in new mexico, and our senator is here, has seen similar successes, as well. they accepted the, you know, the leadership challenge, and to date, 1,143 small businesses with 3,192 employees have been registered, required information within the new mexico exchange. if they all fully enroll with the average number of dependents, that will be a potential total of 8,000 members, and it's just been opened for a very short period. we'll hear more about that. making the aca work the way it was intended is what i intend to try to do. there are others that have different goals. ensuring that these marketplaces work the way they were intended when we passed the act is vital to helping the businesses in our country and families that depend on these businesses to get the help they need to stay healthy, and most importantly, for me as a mother, not just to stay healthy physically, but to be

3:53 am

mentally free of the worry that any day your business is one day away from bankruptcy or your family is one accident away from bankruptcy. there's no price that you can put, in my view, on peace of mind. i don't know any economist in the world that could price it, but i can tell you as a mother, it's very costly. the s.h.o.p. marketplaces need to work so that small business owners can easily and efficiently compare the different plans that are available for themselves, which they were never able to do, and the employees can pick the plan that makes the most sense. now opponents of the law, and there are many, are fixated, fixated, on the problems of the law as opposed to the promise that it holds. i believe this is wrong. these problems, while challenging, are fixable. we've fixed many things in the united states, big things, bold things, and great things. this is something we can fix. and regardless of how we voted

3:54 am

for the aca, whether we liked it or not, it is the law of the land and in my view, it deserves to be fixed, not repealed. we have the responsibility to make the affordable care act work, not because of politics, but because of the people, and this is not about president obama, it's about the people of the united states of america. it's about the millions of small business owners who want desperately to provide quality affordable health care to their employees, who have dreamed about building a business, who love the people that they work with, and they were never able to find something that they could afford or count on. if they did, they had to compromise below their standards, because i know americans pretty well, and they are very generous people. and it's about people like kiwi armstrong from baton rouge, an independent construction worker, he works on big projects on oil and gas onshore and off. because of the nature of his employment, he works on several projects throughout the course of the year and is not a member

3:55 am

of the labor union. in 2012, he got nine different w2s, but the shifting nature of his employment means he can't get coverage through his employments. when he tried to get blue cross/blue shield, they denied him because of type 2 diabetes. because of the affordable care act, he can get coverage on the health insurance marketplace and give him flexibility to work any project he wants without worrying about whether it will provide coverage or not. this is why we're having this hearing today, we're having this hearing to make sure we're doing everything possible to make sure this act works for small business owners and their employees. my goal for this hearing is it will not be an occasion for grandstanding, but an opportunity to focus on the work before us, which is fixing what is broken and to do that, we have to be honest with each other and open to hear testimony about what's working, what's not working, and when we find something that's not working, how can it be fixed?

3:56 am

some of our witnesses today are also small business owners that have yet to realize the benefit that their colleagues and states where these exchanges are working. some of these businesses are in states where the governor's said no, we're sorry, we don't want to help you. i'm sorry you all are in those states, but that's the situation. i'm going to add one thing to the record, there was a study that came out yesterday that i want to put in the record, the tax study, will somebody please hand it to me? i have it here. all right. this study came out this week, the supreme court's aca decision and its hidden surprise for employers. this is about medicaid expansion, and the key finding is, states that do not expand medicaid leave employers exposed to higher shared responsibility payments under the affordable care act. the associated cost to employers could total $876 million to $1.3

3:57 am

billion each year in the 22 states that have opposed. or leaning against or remain undecided. by way of example, the decision in texas to forego medicaid expansion may increase federal tax penalties on texas employers by $299 to $448. now, this is from a completely nonpartisan jackson-hewitt, i think they prepare tax returns. i don't think they are a stakeholder group to anyone, so because of the decision that governor perry made, his decision, not president obama's, is going to cost his businesses more. now i'm going to turn this over to senator risch, he can have as much time as i did, which i think was probably about 20 minutes, 25 minutes, and then we will go to your statements will be submitted to the record and then we're going to go directly to our testimony.

3:58 am

i thank all of my colleagues for coming this morning. >> well, thank you very much, madam chairman, and first of all, i commend you for holding this hearing, probably not for the reasons you think, but certainly, there have -- when you throw hundreds of billions of dollars against the wall, something is going to stick. and to try to use the handful of things that actually have worked in this 3,000 pages of legislation, and nobody knows how many pages of regulations and say okay, well, it's working because this small part is, really is to ignore the overall problem. again, i commend you for your courage in holding this, and more importantly, madam chairman, i commend you for your statement that you helped to design this system that we have today. i suspect that as we go forward, trying to find people who will admit to having some part in this is going to be like trying

3:59 am

to find somebody that admitted voting for richard nixon. there have been -- this has been a catastrophic failure across america, and you talked about the truth and you quoted -- had a quote about the truth, and i would say this, you know, the american people, they don't understand all the niceties and all the complexities of health care and health care insurance and what have you, but they know when they've been lied to, and the polling is incredibly strong indicating that they believe that they've been lied to. and once the american people believe that they have been intentionally lied to, it really causes difficulties in trying to solve problems and this is -- this does not bode well as we go forward. you know, you had your list of, i think, successes there, and one of them was idaho.

4:00 am

when i was governor, i appointed the gentleman who now sits as the director of health and welfare, my successor kept him on, and he's a really good guy, came out of the insurance industry. i'm not exactly sure if you were boasting that idaho is one place where obama care is working, but i can tell you that it is a disaster in idaho, and perhaps it isn't in louisiana, but it is a disaster in idaho. i know that you brought in some people from kentucky to talk about some of the good things, and i believe that kentucky's working better than other places, i'm told, although that isn't a very high bar, but i've got a couple of letters i want to put into the record from insures, who are working in this area in kentucky. and i'm just going to read part of it with an indication of what's actually happening in kentucky. this is from a group, i believe it's hauchens insurance group

4:01 am

from bowling green, kentucky, written by the executive vice president. "we are writing to you to explain what we've seen in kentucky and other part of the countries that our company serves, regarding our clients' implementation of the affordable care act. well, we are not a small company, our insurance group, hig, serves over 1,000 small businesses with their insurance needs throughout kentucky and the united states. the remainder of this letter lays out what we are seeing. for an agency to represent its customers responsibly, we need to be able to share all options available. at this point, kentucky's health care connection, connect, presents us with more challenges than solutions. to date, we have not enrolled any groups in the small business health options program, s.h.o.p., primarily because the confusion the system has created. business owners are anxious and frustrated as to what they have

4:02 am

to do in order to get pricing. creating an account within connect and then assigning an agent takes a considerable amount of time and is not something they should have to do while managing their business." he then goes on to list many more of the problems and i'd like that put in the record, please. the other one comes from the benefits firm, another company in kentucky. and again, the senior vice president writes, "kentucky has been viewed by other states and people in washington, d.c. as a state that most things have gone correctly with the health insurance marketplace. well, it is true that connect has been operating properly, especially compared to the federally facilitated marketplace. there are still many unresolved problems. in particular, i'd like to address the s.h.o.p. exchanges. logistically and technologically, we are not having the same success in kentucky with the s.h.o.p. exchanges as we are with individuals in connect. this week i have reached out to numerous benefit brokers in kentucky, none of which have finished a connect s.h.o.p.

4:03 am

exchange application. while i do believe that the technical end rans is part of the problem, it is not the primary problem of the success. i firmly believe there are flaws to this existence that the current law cannot overcome. numerous businesses that i have worked with decided that with the p.p.a.c.a., there are avera advantages to their business through connect, however, the advantages is to allow each of the individuals and families to enroll in connect." then he goes on to explain why that's a good financial decision for businesses. so, there is no doubt we're going to find some things that happened here that are good, but like i say, when you throw these kinds of hundreds of billions of dollars at it, you're bound to find that. lastly, i'd like to focus on what has been something that is really undermined the confidence of the people of america in this, when the president stood up as many times as he did and

4:04 am

particularly democrat senators stood up as many times as they did, looked in the camera and said, if you like your health care plan, you can keep it. those of us who listened to that the first time said that that's impossible, where the government was going to lay out all these things that they are going to require in a new health care plan, no plan would exist, so i don't know how the president of the united states could stand up and say that and then repeat it over and over and over again when these people had to tell him, policies no longer exist. somebody should have said, mr. president, stop saying that. you're going to get hit over the head with this, and, of course, now the chickens have come home to roost and that's where we are. you know, we tried to change this. my good colleague, senator enzi, introduced senate joint resolution number 39 and we had a vote on september 21, 2010, and that resolution, which would have become the law of the united states said, if you like

4:05 am

your plan, you can keep it, but we weren't able to pass that, were we, senator enzi? there was a straight party line vote with all republicans voting for senator enzi's bill saying just what the president had promised, and every democrat voting against that promise. and it's really unfortunate that it has come to that. well, here we are again trying to apply lipstick to this pig, and no matter how many times it's said, the american people aren't buying it. the numbers are deteriorating every day as far as the confidence of the american people, not only in what's happened here, but particularly in going forward what we're going to do about this catastrophe, and that's a problem, i think, that you and your colleagues are going to have a very, very difficult time wrestling with. and the good news is, we are americans, we are free, we're going to have an election next

4:06 am

november and americans again are going to have a say in this and everybody's going to be able to stand up and say, look, i did this, i helped design this system. i had my hands involved in this, so put me back there and see if i can't do a little bit better next time and american people are going to decide whether or not that's appropriate, and that's exactly as it should be in america. and as with all other issues we've had in america, even though this is a, what someone would call a manmade disaster, we will get through this, we are americans, we know how to fix these problems, and we'll do it. and with that, i will yield back, madam chair. >> thank you very much, senator. let's begin on the panel with our first panelist, and then i'm going to call on senator hinrich to introduce the gentleman from his state, but let me start with mr. william nold, director of the office of kentucky health benefit exchange, then we have mr. david allen, president and

4:07 am

ceo of david allen enterprise. i'm sorry, we're going to go in the order of mr. nold, then go ahead and i'll introduce everyone else. go ahead, thank you. >> chairman landrieu, ranking member risch, we really appreciate -- and members of the committee, we really appreciate -- >> you're going to have to speak into your mic, it's a little bit -- >> really appreciate the opportunity to come over here to d.c. this morning and to share kentucky's experience with our exchange, which we call, senator risch said, we call it connect. it's a combined exchange in the sense that both our s.h.o.p. and our individual is for administrative purposes operates under one name. my name is william nold, and as the senator said, i'm the department executive director of the kentucky health benefit exchange. it's a long title and we have a lot of responsibilities. i've submitted a written statement and also some other

4:08 am

documents i assume will be made part of the record. >> we do, that will be part of the record and you have four minutes and ten seconds. >> my next note is time was limited, but i think a little time should be spent to talk about the landscape in kentucky as it has existed for a number of years. our population is about 4.4 million. 640,000 of those individuals are uninsured. of grave concern to our governor, however, is the health status of our state. we're 44th in overall health status, 50th in smoking, 40th in obesity, 41st in diabetes, 50th in cancer deaths, 49th in heart disease, 43rd in cholesterol counts, 48 in heart attacks. you know, we began our implementation of this law immediately after it was passed,

4:09 am

but as you know, many of the provisions in the law were related to insurance matters early on, and the exchange seemed like it was a far off, you know, 2010 and the exchanges really don't have to be operational until 2014, but we began immediately to try to bring consensus among all the stakeholders in kentucky about what we were wanting to do with this exchange when the time came. to everyone in our state, wanted us to do a state-based exchange, everyone. i think deb mosner, who is the president of anthem in kentucky, probably said it best. she said, if i'm going to be regulated, i want to be regulated across the kentucky river, not the potomac river, and that kind of said it all, i think. although a lot of these stakeholders were opposed to this law, they realized that,

4:10 am

you know, at least until the supreme court would make its decision, that we were stuck with it, and so it's a good thing that we're stuck with it, that's the way we found it, anyway. so, of course, we continue to meet with governor bashir along the way, making decisions about what we were going to do, and so he wanted to wait until after the supreme court had ruled to really dig into this and get moving on it, and that's what he did. and so we presented all the pros and cons to our governor about what we should do or what we shouldn't do, and he kind of stopped us. he said, look, he said, and he's a lawyer, he had read the bill, he said, this bill provides a unique opportunity for kentucky to improve these health statistics. i want you to do everything that you can do to use this bill, not let this bill use me, but to use

4:11 am

this bill to improve our health. and that has been the charge that we have accepted and have gone with ever since. you know, my time is getting short here. i do want to share with you, you know, we went live on october 1st, down for a few hours, not down, slowed up for a few hours, got that all straightened out and we've been running ever since and helping people get enrolled, not only in our s.h.o.p., but also in the individual market. so i guess the message from our governor is that he was very strong in his opinion that the best way we could improve the health of our state was to go the state-based exchange route and then also what we have done is that we have gotten agents involved. right now, 94% of the small

4:12 am

insurance policies in our state, small employer insurance policies, are offered through agents. >> try to wrap up, please. >> yes, ma'am. well, to summarize, and again, this is in particular with regard to the s.h.o.p., since we went live on october the 1st, we've had 193 small businesses that have started applications to be eligible for employee coverage. >> i'm sorry, i'm going to have to stop you there. we have so many people to testify, and i really appreciate, and you have a wonderful statement we've put in the record. thank you, mr. nold, but we're going to have to go to our second panelist, senator? >> thank you, chairman landrieu for holding this hearing on the rollout of the affordable care act small business exchanges. with attention squarely focused on implementation challenges at the national level, a deep understanding of how our small businesses are fairing in securing meaningful, affordable health insurance coverage for

4:13 am

their employees is timely and essential for the economic well being of americans and the -- just an introduction, okay, i'm delighted and honored to be here today to introduce one of our invited panelists, dr. martin hickey. he will describe to you in detail the success of the new mexico shop. dr. hickey's not only a member of new mexico health insurance exchange board, but also the ceo at new mexico health connections, a co-op formed under the affordable care act to provide health insurance to small groups and individuals in new mexico. he's also a general internalist who first practiced on the navajo nation, and he's dedicated himself to developing rural health programs. over the past three decades, he built a distinguished career in health systems administration and delivery system reform across the country and we're fortunate to have him in new mexico. i give you dr. hickey. >> thank you. dr. hickey, please, you've got five minutes.

4:14 am

>> chairman landrieu, ranking member -- thank you for the opportunity to testify today about the early success of new mexico small business exchange. new mexico legislated a state-based exchange board in march of just this year. the board consists of 13 highly representative members of groups, including small business, consumers, native americans, hispanics, physicians, hospitals, health insurers. within five months, the board and its very capable ceo and team, selected an experienced private exchange vendor, developed a state-wide plan for marketing, trained over 500 health care guides, set the rules for open market exchange, and succeeded in launching a fully operational enrollment website, be well new mexico on october 1st. at this time of national glitches and confusing rhetoric, the board, our very supportive

4:15 am

governor, martinez, and all new mexicoens are very proud of the early enrollment successes that i will shortly detail. you got a background on myself. i have been ceo and senior manager in insurance companies, medical groups, hospitals, i have seen this business from every single side, and what i'm so proud of is that i have always dwelled on fixing access to care, and i can tell you that this board that has come together from literally both sides of the aisle in new mexico has come together passionately to assure access to care. new mexico is 23% uninsured, second only to texas, has 200,000 uninsured and 118,000 of them are eligible for financial assistance. and get this, only 47% of the population has employer-sponsored insurance, the lowest in the nation, which has an average of 58%.

4:16 am

our state exchange is unique from most others and we call it a hybrid. because the exchange formed so late, we did not have time to implement an individual exchange this year, we were, however, able to procure a competitive contract with get insured, an information technology. next month they will begin work on implementing the technology firm individual exchange, which will be ready to roll out for enrollment in october of '14. in the meantime, we have had to depend upon the federal exchange, but be well new mexico has a calculator, is educational, and when the federal exchange becomes fully operational, people will be informed. the small business exchange is also unique in that it not only offers employers a choice of plan, but offers choice to each of their employees, as well. the employer enters the site, selects a level and reference plan, the employer designates a

4:17 am

percentage premium that will be covered and then creates that -- that then creates a dollar amount made available to the employee for premium support and whatever plan the employee chooses, thus, the employees have a choice of any plan of any carrier at that level at whatever cost. and that is what is so great about new mexico health insurance exchange for small businesses and their employees, choice, choice, and choice. you know what, even better, it works. and, it's easy. i did it for my family last week and it was like going down a waterslide. there is even a calculator to help an employee choose the right plan based upon generalized use of health care in the past. i think the following quote from a small business in albuquerque, an attorney with 400 employees sums it up best, "i was very pleasantly surprised. i thought it was going to be an administrative nightmare and it literally took me 15 minutes. they gave me a quote that would save me $1,000 over what i was

4:18 am

paying. i thought this was going to be an all-day thing, so i had a diet coke handy, well rested, had a good lunch, and it was almost disappointing it was so easy. i was blown away." so, to date, as you said, senator, 1,143 small businesses in our little state with the number of employees is essentially propelled us to a potential once all the enrollment finishes up by the end of the month of over 8,000 members, which already meets the goal that the board had set for the state, and we've still got the rest of the year and all of next year to go. so, and as i said, we have 500 personal assisters and the brokers are heavily involved, as well, the other thing you emphasized is cost, and our superintendent estimates that the rates for next year will be no more than 5% what they were this year when the american society said it would be a 34% increase, he also set up a very competitive process, i know, i had to go through it, so new

4:19 am

mexico audio ] >> thank you, dr. hickey. my only question is are you available to come to washington? all right. we'll go now to miss -- i'm sorry, let's see. mr. david allen. [ no audio ] >> i'm the owner and operator of flat iron practice management. we're an independent medical billing company in boulder, colorado. we produce services to several hundred health care providers. i currently employ 33 full time personnel. we're well bow low the employer

4:20 am

mandate threshold yet we provide company paid health insurance to our employees anyway under a small group plane an have for many years. we do so because we can and it's the right thing do. i worked as an employee for other companies before choosing self-employment and i relied on my employers for access to health insurance. unfortunately, it's been increasingly hard for me to continue to provide health insurance for my employees. health insurance is the next largest expense. even with annual inflation rates and the 1% to 2% range, our premiums increased every year by 20% or more. as much as i wish i could simply pass this along to my customers, they, too, are experiencing the same pressures to manage rising expenses in their small businesses. we've done some creative things over the years to reduce the magnitude of the premium increases while maintaining the integrity of our coverage. and have been successful in continuing to pay for 100% of

4:21 am

the cost of premiums for our employees. one such tactic was to select an insurance policy that covers only generic pharmaceuticals. anyone who requires a pharmaceutical that is only available as a brand name product has to purchase it out of pocket. as a result of the affordable care act, our carrier discontinued this policy. as it does not meet the minimum standards stipulated under the law. due to this one change our premiums are now scheduled to increase by 52.3% in january 2014. clearly absorbing this expense in order to continue to provide the same benefit to my employees is entirely unrealistic. i will have no choice but to require my employees to contribute substantially to the costs of their premiums. the irony is that none of my employees currently take any brand name prescriptions or expect to in the foreseeable future. this law has turned what was a potential expense for my

4:22 am

employees into a guaranteed expense for my employees for something they neither need nor want. i decided to embrace this and turn to the state shop insurance exchange in hopes it would provide me with more affordable and appealing options. the first obstacle i encountered is the website would not allow me to create an account. after my fourth failed attempt, i initiated an online chat with one of the exchange personnel and told after close to an hour of waiting that they were having technical difficulties with creating accounts and i should try again later. i did eventually create an account and download the census template. i began the frustrating experience of attempting to upload the census. i tried unsuccessfully several times and received nonsensical errors such as wrong file type when the file i was trying to upload is the very template i downloaded from the website. after initiating my second on

4:23 am

line chat, it eventually came out that my web browser might be at fault. i find it unfortunate that website didn't disclose any browser limitations before i wasted i didn't think another hour spinning my wheels. upon switching browsers, i was able to get the website to acknowledge the file that i was attempting to upload but it ultimately je lly rejected the the base thas date of higher field wasn't formatted correctly. my third online chat resulted in validation that my data was in fact correct -- was formatted correctly and the website was, again, experiencing technical difficulties. growing increasingly impatient, i resorted to having my assistant manually type the information into the website. which should have taken us minutes to complete instead took us hours. having finally uploaded the census, i received 34 insurance plan options from which to choose. i found it challenging to compare and contrast them with the current plan and 2014

4:24 am

equivalent because we currently offer tolerable $750 annual deductible and the lowest deductible available to us under the state exchange is $1500. in short, the only way we can markedly reduce our insurance is select a policy with a higher deductible thus shifting the financial burden from me to my employees. i could do this on my own without the assistance of the exchange. instead, we opted to make concessions such as brand name pharmaceuticals. on the surface, my company stands to benefit from the affordable care act on the base thas more people will consume health care services provided by my clients thus resulted in more business for me. but this theory hinges on the availability of the insurance available. if my experience is any indication of the unintended

4:25 am

consequences of this law, it would appear that the affordable care act accomplished the polar opposite of what the law was designed to do. >> thank you. our next witness is mr. drew greenblock. >> thank you. >> please identify your state plchlt allen, just for the record, you're in colorado with state run exchange. that is obviously according to your testimony, has some difficulties. mr. greenblot. what is your state and what kind of exchange do you have? >> maryland state and we have the shop exchange but it is starting in april. >> and is it a federal exchange? >> i believe maryland state is trying to do it on its own. but i'm not positive. >> state-run exchange. >> okay. >> chairwoman, ranking members, thank you for your opportunity -- the opportunity to testify before you to day.

4:26 am

i'm drew greenblatt. i'm pred and owner of marlon steel water products based in baltimore, maryland. we are manufacturers of wire baskets. we make it 100% in the usa. we make it here and ship it to 36 countries and my favorite is we export to china. i'm pleased to testify on behalf of the national manufacturers along the executive committee of the national association of manufacturers. since we're in the small business committee, i thought you'd be interested to know that our average member has 35 employees. 97% of us provide health insurance for our employees. i mention this because the health and safety of our workers is critical to manufacturers. as a matter of fact, my company we hit a huge milestone two weeks ago. we've gone 1800 days without a lost time accident. to the most -- the thing that i'm most proud of in running

4:27 am

this company. this commitment to a safe workplace is critical. to me, offering high quality health care coverage is part of that mix. providing this good coverage is personally important to me because my family is in the same plan as all my employees. so we're all in this together. generally i have come to expect my health insurance costs to go up 8% to 12% a year. i was shocked when our health insurance went up 49% this year. i want to provide health insurance for my employees and their families. we've been doing it for 15 years since i bought the company. but now because it's so high, our plan in effect is not vie ablg because it's not affordable. ultimately, we're able to secure an alternative coverage plan for my employees because our term ended december 1.

4:28 am

my premium, however, is still going up 10%. the plan i purchased includes benefits i don't really need nor do my employees want. this is key. the accordability, it's gone up. the costs have gone up despite all the promise that's our cost was go down. if i told my clients we're raising your prices 49%, they'd laugh at me. 49% is out of control. even if i sat down and explained you'll have new features. they denlt want to hear about it. and this is the environment we're in. i recently discovered the shop exchange in maryland was delayed until april. i'm not sure what products it offers. this is the kind of instability that is harmful to our economy. see, we don't know how much our employees are going to cost this year. we don't know how much it's going to cost next year. how do i quote jobs for my competitors in china? how can i win jobs that are three-year and five-year contracts when i don't know how

4:29 am

much my costs are going to be? i know that the aca law is not going away. any change is going to have to happen through bipartisan legislation. i urge legislators to look at all the laws that are the not working. please fix them. this will not get better with finger pointing. this is not going to get better with rhetoric or regrets of broken promises. we need practical approaches right now. cost was and is remains our main issue. we lu reducing the cost of care makes the system more efficient and impacts the access to coverage. >> please wrap up. you have 56 seconds. >> driving up the cost of coverage and providing subsidies to some just camouflages the underlying problem. i may not be a supporter of the current system, but i would support changes that allow me to continue to provide high quality health care to my employees at reasonable price. thank you for the opportunity to

4:30 am

testify today. >> and thank you, mr. greenblatt for your excellent testimony. apologize. i'm not seeing well with my cold. did you a very good job. i thank you for focusing on fixing it as opposed to the rhetoric associated with another proposal. all right. mr. -- let's see here. ms. salter. >> good morning, madam chair, ranking members and other distinguished members of the committee. i am honored to be here today and to share my negative impact obama care has had on my small business and me. my name is sheila a. salter. i'm the sole proprietor of early to surge. i reside in north carolina and that is a state that has defaulted to the federal exchange. my company is a marketing consulting business. and the mission is to improve or accelerate the development and

4:31 am

commercialization of surgical devices. my primary customers are start-up device companies. now i've been in health care for over 35 years. i'm well aware of the weaknesses and strengths within our health care system. i don't think there is a person in this great country of ours who does not wish for every individual to have affordable health care. obama care has a negatively impacted my business and filled me with uncertainty. i am my business. i planned for many years to have my own business. i invested my time, my money to begin early to surge this past member. now because i have no employees, i'm not eligible for shop at this time. but it would be a reality if and when i could afford to expand. that is in my business plan. now i'd like to direct you to either the screen or you have in

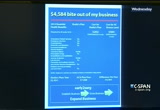

4:32 am

front of you a chart that i had submitted. you know, i was shocked back in september when i received notice from blue cross/blue shield that my health care plan was going to be canceled and it was going to be replaced by one that had been chosen for me at the tune of $584 a month. now if you look at the chart, we all need to be clear on this. there is one health care plan. when i hear people talk about oh, you know, go to the exchange. shop, shop, shop. you have one plan. okay? that plan includes the benefits listed in the left hand column. now you can see sheila's plan. sheila's plan is the one i chose. i chose my services. i've done that all these years. i chose those services, chose that deductible for $202 a month. now, with obama care, i have to

4:33 am

have those ten essential benefits. now i challenge anybody in this room to look at the services that i selected for myself noting that i'm 61. i know i don't look it. and i have no children or history of alcohol or drug abuse. yet. okay? this is driving me to drink. but does anybody here really think that that -- that i need all the services on the left hand column? i don't think so. to have those choices removed from me, to have the government tell me, sheila, this is what's best for you, i really -- i mean shocked is not the word. it is unacceptable. it's unacceptable now. it's going to be unacceptable 12 months from now and i will never accept for someone to make my

4:34 am

health care chakacare choice fo. the only thing the exchanges have done, and i've gone on the exchanges, you have a selection of what's your deductible, what's your co-pay, what you're going to do for prescription. are you going to be in network or out of network? but i don't care if you're a man or woman, you're going to have maternity and newborn care, you're going to have pediatric services and services that you may or may not need. you know, that, i think, there should be a fix to it. i'm willing to work with anyone to fix that. so how has it affected my business? well, it's impacted how am i going to establish my business, growing my business, expand my business? all of that is going to be delayed. and as you know, the website is not working exactly up to par. but i'm concerned with the security of the website. you know, if i have identity theft, any of us have identity theft, we all know what the

4:35 am

sequences of that is. you know, it could wipe me out to the point i would never recover. so, you know, in our business, health care business, we have a motto, first do no harm. first, do no harm. i want to see everybody have affordable health care. that is a given. but, you know, there are some fixes that need to be made and i'm happy to help. thank you. >> thank you very much. miss evans? [ no audio ] >> and welcome back. >> i'm the president and ceo of the association for enterprise opportunity, aeo, the national member organization and voice of microbusiness in the united states. for more than 21 years aeo and its more than 450-member and

4:36 am

partner network of nonprofit lenders and business development organizations have provided critical services, access to capital and business counseling to underserved entrepreneurs and microbusinesses all across the country. the importance of our topic today, health insurance and the value to microbusinesses, cannot be overstated. similarly, our discussion of how certain elements of the affordable care act are changing the health care landscape cannot be timelier. before we proceed to the topic, however, i would like to give the committee some statistics about microbusinesses, those businesses with under five employees that aeo released just last week. the report bigger than you think, the economic impact of microbusiness in the united states, tells a powerful story of how the nation's smallest businesses make an contribution to our economy. there are 26 million microbusinesses in the united states or about 92% of all

4:37 am

businesses. the ripple effect of direct, indirect and induced economic activities of these firms is quite impressive. total employment of 41 million americans, total economic impact of $5 trillion and total revenue contributions of $135 billion to federal, state, and local governments just in 2011. in other words, although the main street businesses are small, they're combined impact is quite significant. despite advantages, however, many would-be entrepreneurs are hesitant to leave their jobs. for decades the inability to obtain health insurance has been a barrier for those interested in starting a business. it is well documented that access to health insurance drives employee decisions. before the aca removed pre-existing conditions as a barrier to obtaining health insurance, employees often chose

4:38 am

to stay with employers even though they were unhappy with their employment. it prevented those who might have otherwise left their jobs to start businesses. as the chair expressed this morning, the robert wood johnson foundation does project 1.5 million americans including 25,000 just in the chair's home state of louisiana will become self-employed thanks to insurance reforms and the affordable care act. the entrepreneurs and microbusinesses, aeo member's serve have the unfortunate choice of hamstringing the revenues by providing health insurance to employees or losing employees to larger companies who can provide that insurance. the aca reforms to the health insurance market in our opinion were necessary and we hoped that these changes would lead to better prices and more choices. our optimism is based largely on

4:39 am

the exchanges, also referred to as new marketplaces which allows individuals or small businesses to pool together to obtain insurance. it is with profound disappointment that the program is in complete disarray. while most of the cost's attention is focused on fixing the shid exchange, the small business exchange or shop has been treat the as a secondary concern. we fear that implementation of the federally facilitated shop will continue to suffer delays. even though the law requires individuals o obtain health insurance, many plans for individuals and businesses end at the end of 2013. the decisions about coverage have to be made whether or not the federal government can successfully rollout the exchanges. we note that many individuals have received notices saying the coverage will be discontinued because that plan does not comply with the aca and the insurance companies have advised

4:40 am

these customers to shop in the exchanges. but of course the exchanges are not up and running so there is much frustration over what to do in the meantime. do they just go without insurance and allow a gap in coverage? what do they tell their employees? in closing, our message is not based on any political leaning or philosophical notion regarding health insurance. we just want it to work. we urge the congress and the administration to come together to make it work for the 26 million microbusinesses on the front lines of our economy. thank you for the opportunity to appear before you today. i look forward to answering any questions the committee may have. >> thank you very much. thank you for your testimony. i'm going to take five minutes for questions. we'll do a five-minute round. alternating. oh, i'm sorry.

4:41 am

i am so sorry to miss you. i tell you, this cold is really knocking me for a loop. go right ahead. ms. kauffman. >> thank you very much, madam chairwoman. thank ranking member senator rish and members of the committee. my name is neila kaufman. i'm the executive director of the district of colombia's health benefits exchange authority. otherwise known as dc health link. thank you so much for your leadership and advocacy on behalf of the nation's small businesses both for your home state and nationwide. it is truly appreciated all the work that you have done through the years for the small business community. it is my honor to be here today.

4:42 am

in march of 2012, mayor gray signed legislation creating the d.c. health benefit exchange authority. we are a private-public partnership with seven voting members who are small business owners and experts in health insurance and health care financing. we also have four government members who serve as nonvoting. in the district, it really does take a village to bring success to date. we had a very strong partnership with all of our agents, government agencies. we also had a very strong partnership early on in our policy decisions. we had policy work groups, stake holders who helped us make our policies and set our priorities.

4:43 am

we had the political support we needed to move forward. we also had strong relationships and collaboration with the business community here in the district. business associations who represent the small business owners here. and we also have strong support from the federal government and especially gary cohen and his entire team. on october 1, we opened for business. as you know, it was reported that we were one of four states that opened on time and did not go down. and we have not gone down. we are fully open for business and we welcome everyone, every individual who lives in the district, every small business that is in the district and now i look forward to serving many of you and your staff and it was a great pleasure to be designated as a provider of health benefits to all of you.

4:44 am

we had very strong partnerships with our insurance industry. we have four major insurance companies selling to small businesses through d.c. health link. and i think that the best insurance companies in the nation, aetna, united, care first blue cross/blue shield and kaiser. they offer 267 different products to small businesses, something for everyone. if you want zero dediuctible plan, it's there. if you want a high deductible plan, it's there. it's all price points. our carriers offer nationwide position and provider networks and very robust local and regional networks. and we are very proud to offer full employer and employee choice. so when a small business comes in and it's very easy to create

4:45 am

an account at d.c. health link.com is our web address, when a small business comes in, the small business decides how much to contribute and what options to offer to employees. for the first time a small business can offer the types of option that's only in the past have existed for the large employers. a small business can pick what to contribute and pick a level of benefits like the gold level and employees have 112 different products to choose from. and the small business gets one invoice. we clearly say how much the small business has to contribute. and how much to withhold from the paychecks of employees. we also did not -- we decided to take advantage of the private market innovation. so we did not negotiate rates or benefits. we let the insurance companies compete and boy did they compete. after we made all of their

4:46 am

premiums tub lick, one company came back in lowering their rates twice. a company came in and lowered the rates one. and eye third company came in and lowered rates and offered additional products. [ no audio ] when insurance companies compete, small businesses and individuals benefit from that competition. i want to note that -- >> will you try to wrap up? >> i just want to note and thank d.c. chairman better of commerce and the hispanic chamber of commerce and the restaurant association of the metropolitan washington area. they have been our strong partners. and they are part of our success. i look forward to answering any questions you may have. >> thank you very much. before i start my line of questioning, i'd like to submit

4:47 am

for the record a letter from the state of minnesota, the governor mark dayton who was a member of the senate. he quotes, and i'll put the rest in the record, "mn surs focus is to create a minnesota made exchange that best provides for the needs of minnesotans. virtually every health care organization, business organization, respected expert strongly supported our state exchange and designing something that would work for us." he couldn't be here. minnesota couldn't testify. but they have some excellent information. let me, and i'd like to submit to that to the record with no option. let me respond in my time first to my good friend and ranking member's reference to my not supporting senator enzy's amendment. he can certainly explain his amendment. i want to say the reason i voted against it and every member of the democratic caucus is because

4:48 am

it would have eliminated the cap on lifetime limits. people could exceed their limits and would have knocked young adults off their parents' plans which is one of the strongest features of the affordable care act. i say senator enzy can defend himself and his rebuttal. his bill, which i voted against and many democrats did not keep the promise it gutted the bill. now i have a bill that will actually keep the promise and last week in the house of representatives both republicans and democrats overwhelmingly voted to support some version of the keep your promise bill that would extend that for a year. that would help you because you could actually keep your plan. so i want to put that in my record. the first question is to you, when did you start your current

4:49 am

business? >> i just started february. >> so you've been in business nine months. and you're just starting. i want to put into the record that not only if my bill could pass and i hope can you support it or a version of it, you can keep the plan that you want. but if you chose to go to another plan, if you make 2$27 thou,5 hun -- $27,500 a year, you'll save $596. if you make $32,000 a year, your annual cost of your premium, even in north carolina where the state itself chose not to help you by setting up their own exchange, they let it be set up by the federal government. so your state made that decision, not us.

4:50 am

you would save -- you would pay every year $919 and you'd save $4,257. if your business makes $35,000 in your first year and it goes up to 40 or $45,000, your premium, you would still save $2,823. so i'm sorry that your exchange is not working well. but there are some benefits that hopefully you can come to appreciate as we move forward. let me ask you, miss kaufman, you know, d.c. exchange has gotten some very good feedback. as you said, both bipartisan, republican and democrat. it's understood. what would you say are the two most important features that caused your exchange to be so beneficial to your small businesses? was it the way it was designed? was it the cooperative nature? what was it? and what would you recommend to others trying honestly to fix this and to make it work for

4:51 am

their small businesses? >> thank you, madam chair. there were several elements that were critical to us. we wanted to build the xlafrpg from the ground up, community based effort. priorities, policies that we adopted were very much stake holder driven. and the decisions we made reflect the stake holders who were involved in helping us build d.c. health link. the other pretty call part to us is the huge choices that are available to small businesses. 267 different products, everything, hmos, ppos, no deductible, high deductible, everything from all of the major insurance companies. and our value proposition is we want to make it as easy as possible to small businesses to be able to offer coverage and offer small businesses the kind of clout they never had in the

4:52 am

past. and that as well as the business community in the district stepping up to the plate, putting politics aside and helping us make hard decisions and helping us to build this, d.c. health link to provide service that's small businesses need and want and are desperate for in terms of affordability and predictability and an opportunity to offer great options to their workers. it took a village and the small business community was a part of it. >> thank you. >> madam chairman, back to the enzy proposal again, i heard your explanation. you voted against it because it eliminated lifetime caps that was required under obama care and eliminated the 26-year-old coverage which was required under obama care. but that this is exactly the

4:53 am

point. you didn't promise us that if we politicians like your policy, we're going to let you keep it. you said if you like your policy, can you keep it. there were a lot of people that wanted to buy policies that cost less and that didn't have lifetime caps lifted. there are a lot of people that wanted to buy that didn't cover their 26-year-old. you didn't let us do that. and that is the problem. we are smart people. we can make our own decisions. we don't need the government telling us what we have to have. and that is the biggest complaint i get from idahoans, from americans saying why are you politicians and washington, d.c. constantly telling us what we should do for ourselves? and that's the basic problem of all of this. whenever you try to socialize in the industry, nationalize an

4:54 am

industry like it's been done here, it's never worked. it's been in tried in all sorts of countries and it never works. it's not going to work here. well, let me go over a couple other points. first of all, i want to ask mr. knoll, i'm told that there are -- have been 150,000 small group plans that have been canceled in your state. is that true? >> sir, i'm not familiar with the number there. the department of insurance is the agency that handles the mechanisms for that. i'll be glad to provide that information to you. >> i got it. they said there is 150,000 small group plans that have been canceled. on the other side of the ledger, through november 8th, 309 have signed up again.

4:55 am

that's a big problem it seems to me. we have 150,000 canceled and 309 signed up. >> certainly with the small group, it's to note that the open enrollment period that affects individuals is not the same with small groups. there is a continuous open enrollment period available to small groups. they can sign up any time during the year. >> it's really encouraging to hear you were one of five that made the rollout work on october 1st. >> in the morning of october 1st, bloomberg news was reported we were one of four jurisdictions. >> four? >> that went live without a glitch. >> that is really good to hear that they were able to sign up. they were able to get on and do what they wanted to do. that is a really good thing. what is the population of the district? >> we are a small population

4:56 am

jurisdiction. about 640,000. >> i'm told that in the first month with you up and running, no glitches, everything is working good and that kind of population you had five enro enrollees in the first month. is that true? >> no, that's not true. >> what is the number? >> i can provide your office with the exact numbers. we did issue most recent numbers as of november 13th. we had close to 700 employer accounts created. in terms of individual who's completed their applications, both for premium reductions and full premiums, we were at about 1,350 for full price applications. and close to 2,000 for reduced price. each application could be a familiar live ten. we only count applications.

4:57 am

in terms of account holders who collected a plan, over 1100 account holders selected a health plan. and 565 account holders said they wanted to be invoiced to pay. now they're not required to pay until december 15th. so i just want to make sure that people who are residents of the district are reminded of that. we're not asking for people to pay early. we're just -- if they want coverage to be effective january 1st, they do have to make their payment by december 15th. >> so my calculations then is you're a little under 1% signed up of the population of the district. would that be fair? >> i can provide you better numbers. right now folks who are shopping and making decisions, there's a lot of activity through dchealthlink.com. i'm encouraging small businesses

4:58 am

to take their time selecting health insurance. it is not an easy decision. and if you're not not working with a broker who can help you through it, you really do have to take your time. i can tell you as a former insurance regulator myself, insurance is very complicated. consumers who get 150-page document which is their insurance contract which has the exclusions and what is included is very complicated. so although we've made it much easier through our web page to shop and compare apples to apples, we provide four-page coverage summaries that make it much easier than before. it is still not a quick decision. we encourage everyone to take their time. >> thank you. senator booker, let me welcome you to this committee. let me welcome you to the united states senate. i look forward to your leadership. you've already been a champion of small business. you're a perfect person to join us in our effort to help them.

4:59 am

>> thank you very much. >> thank you. this is such an important issue for the state of new jersey that i'm very iestions to greenblatt, appreciate your connections to jersey. you have some jersey boy or a to you. you rock not because of your jersey connection, but i feel a kinship with you. i'm going to stick it out here and battle it out. you deal with pragmatism that idea with. i cut 25% of my employees is a

5:00 am

mayor. one of the reasons i had to do that was because of health care costs. the challenge that you have, which i have seen with local manufacturers, is that you said you export products to china, right? i like you a lot. when you come the globally, you're competing against countries in europe and asia and across the globe, right? many of those countries have health care systems. many of those countries have much lower health care costs, right? [indiscernible] system, butf the their taxes are 15%, our taxes are 40-something percent. >> i want to compete with everyone but toronto.

78 Views

IN COLLECTIONS

CSPAN Television Archive

Television Archive  Television Archive News Search Service

Television Archive News Search Service

Uploaded by TV Archive on